For most Singaporeans, the biggest pushback when it comes to home loans is their fear of taking a bank loan and the perceived difficulty of managing it. Clive Chng is an associate director at Redbrick Mortgage Advisory and he is known for his passion in property financing and building meaningful relationships with his clients.

Clive understands how daunting it can be when you are making decisions without the right information and advice. Here are some myths around bank loans that you might have heard, and Clive will show you the facts that will prove otherwise.

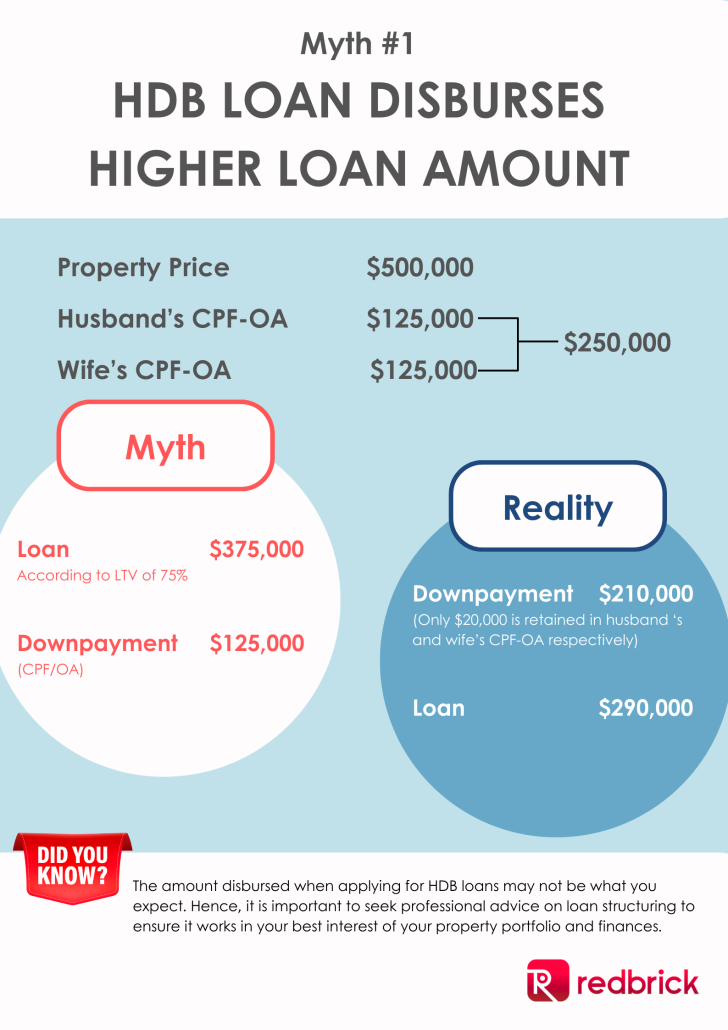

Myth #1: HDB Loan Disburses Higher Loan Amount

Although most people think that HDB would issue loans at the Loan-To-Value (LTV) ratio of 75%. HDB mandates buyers to use more of their CPF OA savings to pay for the down payment, before determining the loan amount.

Currently, each individual can retain up to 20k in their CPF OA while the remainder will be deducted for down payment of the HDB, and only the remaining costs would be disbursed as a loan.

In comparison, a bank loan could allow greater savings in CPF. Using Mr. and Mrs. Tan as an example, should they secure a bank loan at LTV of 75% at $375,000, they would only need to fork out 20% (i.e., $100,000) of the property value from their CPF. This means that they can retain up to $150,000 in their CPF-OA.

Why does this matter then?

Well, in the case where your OA has been wiped out, your monthly mortgage instalments will be based on your monthly contributions to your CPF-OA. Covid-19 pandemic has demonstrated the dangers of job insecurity. Should you be unfortunately retrenched or taken time off for a sabbatical, you would need to dip into your savings and finance your monthly mortgages with cash. This could be challenging given the strains placed on your finances.

To make matters worse, selling your HDB might not solve your problems. For homeowners that have used monies from their CPF to pay for the property, they need to refund the monies used and the accrued interest at 2.5% interest rate upon the sale of the property. The danger is when you make a negative sale or are unable to fully repay your CPF after selling property. If you think it sounds far-fetched, you might be surprised to learn that over 4,500 people were unable to fully refund their CPF monies used after selling their properties and has been on the rise since 2018.

Experts point towards the substantial mortgage sum over a long period of time of more than 10 years and other fees (such as legal fees, conveyancing fees) could amount to a hefty sum.

Despite this, it does not mean that you need to top up cash to your CPF for the difference. Going back to the earlier example of Mr. and Mrs. Tan, they could have made a negative sale when they chose to sell the apartment 10 years later. Let’s ignore the other fees in this case and assume an overall appreciation of 10%.

| Property Sale Price | $550,000 |

| Outstanding Mortgage | $250,000 |

| CPF Used + Accrued Interest | $350,000 |

In this case, their cash proceeds from the sale of their property can only repay for $300,000 of the CPF monies used after paying their outstanding mortgage.

Do they need to top-up the $50,000 using cash?

Well, this depends on HDB’s valuation of the property. When the buyer of their resale flat requests a valuation from HDB on the value of property. If the property is valued at $550,000 and matches the selling price, Mr. and Mrs. Tan would not need to refund $50,000. However, even if there is no need to top-up using cash, the harsh truth is that there may not be cash proceeds for you to keep even if upon sale of your property.

Just remember, the more monies you use from your CPF, the more you have to repay in the future, which raises the probability of having a negative sale. In fact, this could be an issue if you were planning to upgrade from HDB to condominium.

Myth #2: If I default on my HDB loan, HDB will not foreclose my property

It might surprise you, but many believe that even if they default on their HDB loan, HDB will be more forgiving and would not foreclose their property. In comparison, we have all heard stories of banks foreclosing on properties that have been defaulted with absurdly high interest rates.

But doesn’t this sound too good to be true? If this is true, then everyone will exploit the loophole and choose to buy HDB under the HDB loan only to default on the loan. The authorities would fall into a huge deficit simply by this scheme alone.

Truth is, HDB acts like a financial institution (like any other bank) when a borrower defaults. Although they are a statutory body, they will still impose higher interest rates on late payments and foreclose properties in severe situations. Yet, there is less publicity on this issue.

The next question would then be – does HDB have the right to do so?

Technically, when you have mortgaged your home to HDB, HDB has the first charge and has the right to claim the proceeds of your sale first. Upon your failure to repay the loan, HDB can sell your house & use your proceeds to pay off what you owe.

HDB will dispose of your flat and offer to move you to a rental flat instead.

Of course, borrowing from a governmental body also has its perks. One of them is that you get more options if you are struggling to repay your HDB loan. You can choose to add your children as joint owners of the property if your children are working adults, which can help alleviate your finances as your children can help to service the housing loan.

However, your children may face issues with owning a property of their own in the future. Under the current HDB regulations, individuals cannot own more than 1 HDB. This means that your children would need to appeal to HDB to remove their name from existing property. Given the poor credit history of the existing property, HDB might refuse the appeal, and there are generally lower chances of approval. Even if the existing property is sold (and the issue of owning a HDB is resolved), the poor credit history may mean your children would have to pay higher interest rates in future mortgages they apply for.

Myth #3: I cannot use monies from my CPF

account for the monthly repayments if I choose to take a bank loan

Another common misconception that has led many clients choosing to stay with a HDB loan is because they believe that they cannot repay their monthly mortgage instalments if they take a bank loan.

Aside from this, many also think that the down payment of 5% cash and 20% CPF that is typical of bank loans applies to refinancing loans. These two examples are simply a myth. Such regulations only apply to mortgages upon purchase of a property, and not apply to refinancing loans. Also, you are able to use your CPF for your monthly repayments after switching into a bank loan.

Conclusion

There are numerous small misconceptions in the market that have led many to choose HDB loans, but this may not be the most financially prudent choice. Bank loans can offer you better personal cashflows and could offer you greater liquidity to make your money work harder for you. On the other hand, HDB loans could be useful if you have little savings and lack cash on hand. In this case, being able to tap on your CPF-OA for down payment and having lower initial cash outlay could be a more judicious decision.

Nonetheless, if you find yourself uncertain on which course of action is more suitable for you, feel free to approach any of our advisors for more information and for personalised advice.