While every Singaporean talks and dreams about owning multiple properties across the sunny island, and then retiring comfortably on the stable stream of rental income – how many actually achieve it?

And why is it tough for those who are struggling to achieve it?

As for majority of the population, after saving the bulk of your salary for years to finally be able to put the down payment on your first property, congratulations! You have now successfully landed yourself in the biggest debt of your life! It makes it so much harder to save up for the down payment for subsequent properties-to-come as you will now be tied up with your first mortgage.

Also, with the cooling measures in place, the above mentioned dream is shattered for most. Today, I’ll share a little more on what I find is an alternative way to kick-start this journey. For a start, the entry to this highly sought after way of life is to first get a dual-key unit.

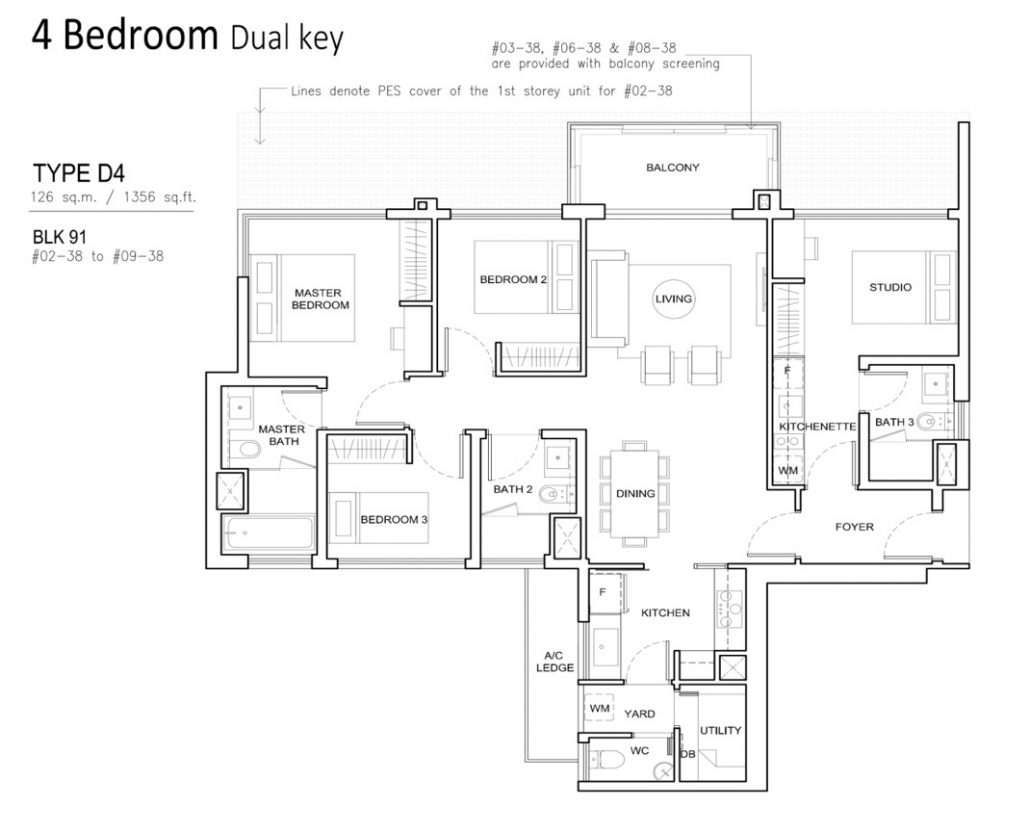

What is a Dual-key unit?

First introduced in 2009 to the private property market, dual-key units are two homes sharing a common main door and foyer under a single title.

Most commonly seen is a studio attached to a 3- or 4-bedroom unit, and there are various ways in which this feature is beneficial to the owner. Let’s take a look at some examples.

Scenario 1: Newly-wed couple and their parents can stay together without compromising on privacy.

There are many perks to having your parents staying with you, especially for newly-weds whom are planning for kids. There are no better nannies than your own parents who had brought you up, they will know what is good for your precious little one(s), not forgetting the joy your parents get from looking after their grandchildren.

There are also other perks such as having warm and hearty home-cooked food every day after a long day at work; it also puts aside other worries such as the perils of aged parents living alone in their own homes.

Now comes the monetary benefits – your parents can then rent out their existing home and have their own source of income! If the rental is good, they may even split it with you to help cover part of your mortgage. Win-win for all!

Scenario 2: Couple with no plans for kids (at least in the near future), a bachelor or bachelorette living alone.

Since you’re living alone, or with your partner, a studio is likely sufficient – and you can then rent out the 3- or 4-bedroom unit. And since it’s a bigger unit, the rental income is most likely able to cover the entire mortgage monthly instalment!

A few years down the road, should you require a bigger living area assuming there are new additions to the family, you can then move over “next door”, and have the studio rented out instead.

Scenario 3: Currently staying with parents and would like to maintain existing arrangement, at the same time looking out for an investment property.

Why look out for an investment property when you can have two?

Not exactly two units but with a slight premium, you get a studio and a 3- or 4-bedroom unit without having to pay for the Additional Buyer’s Stamp Duty (ABSD).

Why is a Dual-key unit ideal?

At the end of the day, why should you consider purchasing a dual-key unit? Firstly, both units come under a single title deed. Thus, there would not be any imposition of ABSD. This allows you to have more flexibility when you’re planning for future purchases.

Being able to collect rental income from your first property will help with the cash flow and financial planning for the second property (maybe even another Dual-key unit?). With rental income being able to cover most, if not the entire mortgage instalment, it helps tremendously with saving up for the second property. You need not fork out extra to pay your mortgage, and you can continue saving your salary for the next down payment.

Due to the desirability to investors as well as the fact that they are still a rather new concept, Dual-key units are usually priced at a slight premium. But more often than not, this is usually offset by the boosted revenue potential.

Finally, don’t forget to keep your finances in check and ensure your affordability before putting your money down on a new property!